| As Chinese President Xi Jinping concludes a two-day state visit to Russia where he met with Russian President Vladimir Putin, SIPRI’s Siemon T. Wezeman puts China, Russia and the shifting landscape of arms sales into focus.

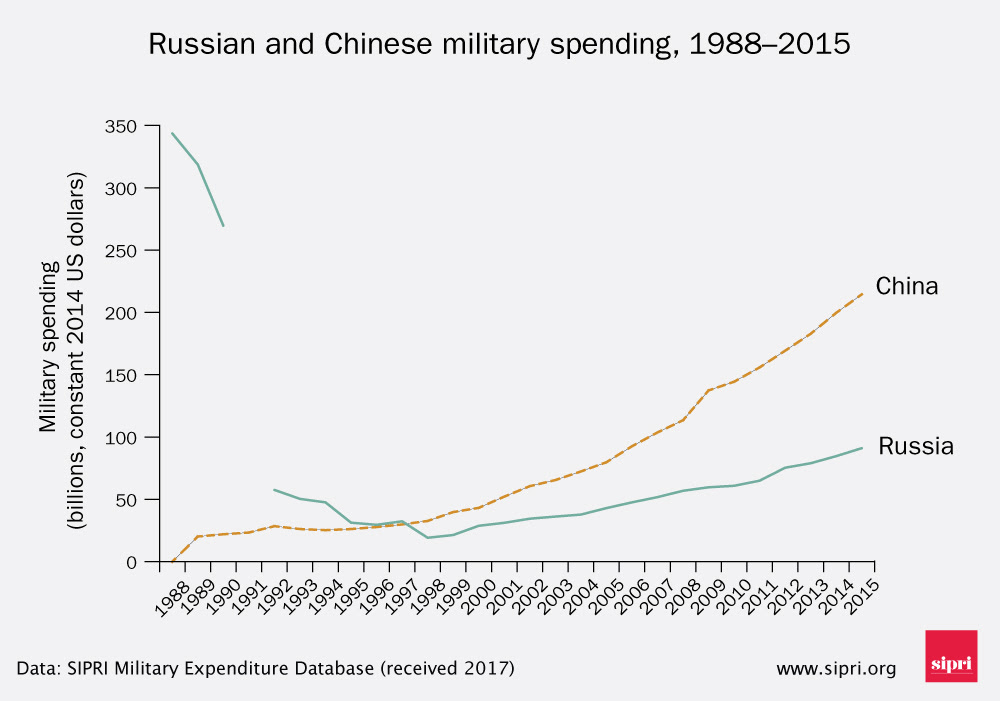

Following the end of the cold war and the break-up of the Soviet Union, there were rapid decreases in Russian military budgets. Soviet military expenditure had stood at almost USD $350 billion in 1988. However, by 1992 it had fallen to USD $60 billion and in 1998 was only USD $19 billion. The more flexible parts of the budget suffered the most, such as those for procurement and operations. At the same time, the Russian arms industry saw several major clients for its weapons disappear, chief among them the former Warsaw Pact members and Iraq. By 1992, the arms industry Russia had inherited from the Soviet Union was in serious trouble. Most of its internal market and part of its export market was gone.

In parallel with this development, China was embarking on a serious military modernization. Boosted by its rapidly growing economy, it began to implement a long-planned reorganization of its armed forces and the acquisition of advanced weaponry. (This modernization had been planned since the 1970s and was given extra impetus by the poor performance of China’s armed forces against Viet Nam in 1979.) Chinese military spending has increased almost every year since 1989, the first year of Stockholm International Peace Research Institute (SIPRI) data for China, from USD $21 billion in 1988 to USD $215 billion in 2015. With this surge, China overtook Russia’s spending in 1998 and within five years had become the second largest spender globally behind the United States.

|

|

|

|

Russian and Chinese military spendng 1988-2015. Data and graphic: SIPRI |

|

Mutual export and import dependencies

Because Chinese arms design capabilities had been relatively stagnant since the late 1960s, based on outdated Soviet designs and technologies, its industries sought the help of foreign suppliers and designers of equipment and components.

In the 1970s and 1980s, these specialists came primarily from Europe and the USA. However, these Western sources were largely closed off in 1989, primarily due to events in Tiananmen Square. Under these constraints, China began a search for alternatives.

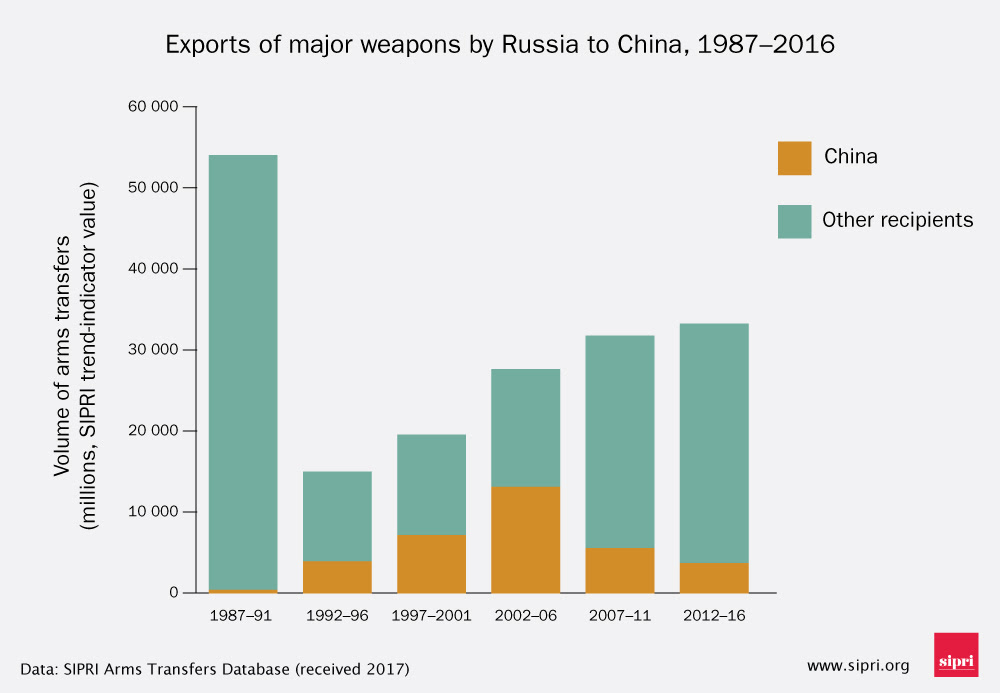

By coincidence, rather than design, Russia and China found themselves in desperate need of a market and a source of military equipment respectively. During the 1990s and early 2000s, Russia’s arms industry survived largely because of its exports of newly produced combat aircraft, armoured vehicles and warships. China played a crucial role during this period. China was Russia’s largest client between 1999 and 2006, accounting annually for 34–60 per cent of the volume of Russia’s exports of major weapons.

| |

|

|

|

Exports of major wepaons by Russia to China 1987-2016. Data and graphic: SIPRI |

|

The decision to sell weapons to China, however, was not without opposition in Russia. There were warnings that Russia would be arming a potential adversary that many suspected had its eyes on the Russian Far Eastern Federal District. Moreover, concerns were expressed that China would copy, without permission and without paying royalties, whatever Russia delivered. In the longer term, worries grew that China might soon become a serious competitor in the global arms market, often in the same countries and regions as Russia. However, the fact that China needed significant numbers of a variety of weapons—and was willing and able to pay in cash—won the argument. At its peak in 2005, China accounted for 60 per cent of all Russian deliveries of major weapons.

By 2006, however, the mutually beneficial export-import relationship between Russia and China had begun to shift. China’s share dropped to below 25 per cent between 2007 and 2009. Moreover, since 2010, the share has halved again to approximately 10 per cent. By that time, however, Russia had consolidated some of its other traditional markets in countries such as India and Algeria and received large orders from newer markets, such as Venezuela. Improvements in the Russian economy also meant that its military spending began to allow for larger orders for its domestic arms industry, reducing the need for exports.

Reverse engineering and market shifts

China’s shift away from Russian exports was in part linked to its own growing manufacturing capabilities. In line with Russia’s original concerns over the potential for reverse engineering by China, copies were made without permission of a variety of Russian weapon systems. Just a few years after Russia delivered the Sukhoi-27 (Su-27) combat aircraft, for example, China released the Jian-11 (J-11). While this aircraft was labelled ‘indigenous’, it was a near-copy of the Su-27. Similarly, new Chinese surface-to-air missiles (SAMs) looked very much like S-300 platforms from Russia. Moreover, Chinese submarines sported features of the Russian Project-877 and Project-636 Kilo class submarines supplied by Russia.

China also started to field its own advanced weapons, such as the Jian-10 (J‑10) and J-11 combat aircraft, various air-to-air and air-to-ground missiles, and several types of warship. Thus, the emphasis of Chinese imports from Russia switched from complete weapon systems to components, such as engines. Only in the field of helicopters were Chinese efforts to develop indigenous systems slow, mainly because China had not yet mastered the production of propulsion systems, such as engines, transmissions and rotors. In this one area, imports of helicopters from Russia have remained significant.

Beyond the diminished need for Russian imports, China also rapidly transitioned into a major arms exporter. This resulted in Chinese forays into markets in which Russia was active, including Algeria, Nigeria, Venezuela, Indonesia and even the former Soviet state of Turkmenistan. (India and Viet Nam are the only important markets where Russia does not face Chinese competition.) Compounding initial Russian concerns over reverse engineering and loss of market potential, China’s L-15 supersonic training and light attack aircraft and the Hongqi-9 (HQ-9) SAM system have also shown signs of ‘borrowing’ from Russian weapons.

New phase or last spasm?

After almost five years of difficult negotiations, Russia and China moved to a new level of arms trade in 2015. Russia finally agreed to sell China 24 Sukhoi‑35 (Su-35) combat aircraft and four S-400 SAM systems for approximately USD $7 billion. These are currently among the most advanced weapons Russia produces. This agreement marked a turning point. It was the first significant sale of Russian major weapons to China since the mid-2000s, representing a sizeable addition to Russia’s total annual value of arms exports, which has hovered between USD $13.5 billion and USD $15 billion in recent years.

The agreement could herald a new phase of large sales of Russia’s most sophisticated arms to China. However, it could also be viewed as a last chance for Russia to gain some income from arms sales to China before the latter becomes self-sufficient. The first scenario would fit the picture of warming Russian–Chinese relations, following the crisis in Ukraine. The second scenario is more tightly bound to Russian financial hardships and the difficulties in its arms industry since 2015. This sale could well be the last chance for Russia to engage in a major sale of military equipment to China. At the same time as the Su-35 and S-400 are due for delivery, China will be introducing its own more advanced Jian-20 (J-20) combat aircraft, as well as its own advanced jet engines, large transport aircraft, helicopters and long-range SAM systems—many of which are on a par with or even better than Russian systems.

When it comes to the arms trade, China has not only learned from Russia, but succeeded in challenging it. Given its financial and defence industrial base, China is likely to have more chances to develop new military technologies than Russia. China’s electronics, composites, advanced materials and shipbuilding industries are all more advanced than those in Russia. The size of the Chinese economy means that it has many more resources and much more manpower to invest in research and development. Thus, it is more than likely that China’s military technology will surpass that of Russia on all levels.

About the author

Siemon T. Wezeman is a Senior Researcher with the SIPRI Arms and Military Expenditure Programme.

Stockholm International Peace Research Institute (SIPRI)

SIPRI is an independent international institute dedicated to research into conflict, armaments, arms control and disarmament. Established in 1966, SIPRI provides data, analysis and recommendations, based on open sources, to policymakers, researchers, media and the interested public. |

{kind=link}